The Hidden Hand: How Macros and Policies Shape Markets

Policy Tailwinds

Can investors ignore macros and government policies to focus on company fundamentals alone? Changes in macros and government policies can provide a strong tailwind for some sectors. These policies create an altogether new business economics for the industries to earn attractive returns. They can bring in competition or eliminate it. We will see a few examples :

India’s thrust on local defence manufacturing :

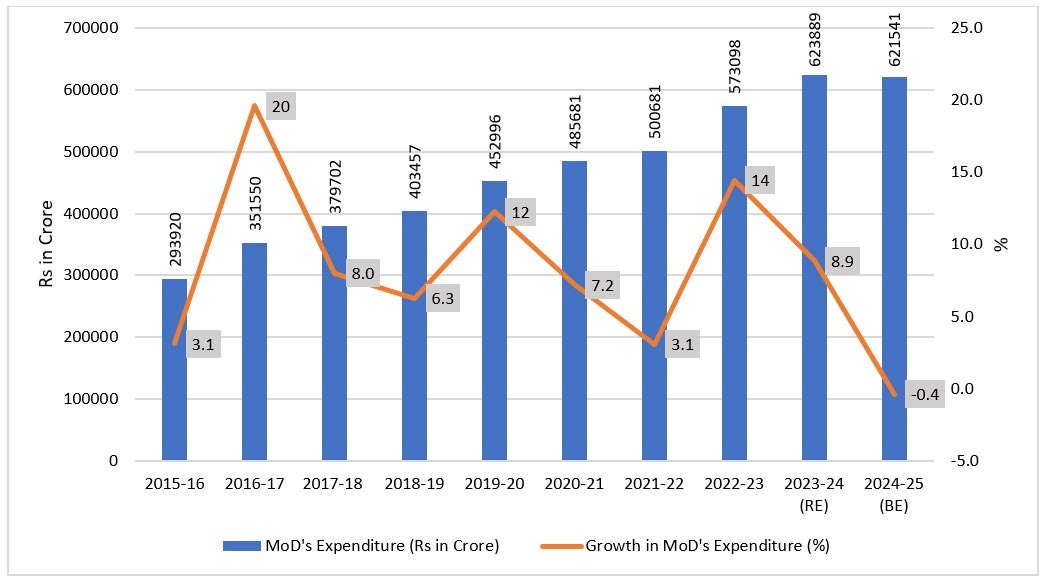

India’s defence budget in 2019-20 was increased by 10% to ₹448,820 crore which accounted for 2.88% of the GDP, highest percentage allocation of GDP since 2009. Similarly, in the budget for 2020-2021, the allocation was increased by 9% and in 2022-23, it was again increased by 10%. However, the biggest increase came in 2023-24 of 13%.

The Government had made it amply clear that it wants to promote defence manufacturing in India. Below image depicts the actual expenditure incurred by the Government. It shows that since FY 2019-20 the Government has increased budget expenditure by CAGR of 9.2% over the next five years. Before 2019-20 also, we saw significant increase in defence expenditure but most of it was for implementation of One Rank One Pension and imports. Since 2020, the Indian Government emphasised local defence manufacturing.

Before the dream rally in defence stocks, they were shunned by the markets due to poor execution, order flow and lumpy earnings. With the Government's change in policy to manufacture in India, timely payments and focus on execution, the business economics for defence companies changed drastically. Investors lapped up the shares. If an investor wanted to make outsized returns he needed to identify the change in stance and increased budget allocations early on. A trend in stock markets starts and ends before it is actually seen in financial results released by the companies.

Revival of state electricity boards and impact on their financiers :

Another theme that played out successfully was of power financiers. The government wanted to expand power infrastructure to boost power production capacity and achieve its target of taking power to all households.That required state DISCOMs to have improved financial health. The government announced packages to help them and these were to be funded by PFC and REC. These were goal based packages. If state DISCOMs failed to achieve the targets they would have to face consequences. With state DISCOMs getting into better health, the performance for PFC and REC improved. The government also focused on building renewable energy capacity and these two entities were prime financiers for the same. They were also allowed to venture into the infrastructure financing segment. Below image depicts the growth in advances for PFC and REC. Before the policy both stocks were trading at below book values. Both got re-rated later and now trade between 1.5x and 2.0x book values.

Substitution theme :

One more theme that caught investor’s fancy was India's Ethanol Blended Petrol (EBP) Program. It is a government initiative to mix ethanol with petrol to reduce vehicular emissions, strengthen energy security, and support local farmers and enterprises. The biggest beneficiaries turned out to be the companies like Praj Industries and Triveni Turbines that provide the equipment, engineering for setting up an ethanol plant. Revenues and profits for Praj Industries compounded at a CAGR of upwards of 25% over the last five years and for Triveni Turbines upwards of 15%. Stocks of both companies have compounded at CAGR of 50% over the last five years. Solid growth in earnings along with re-rating of the stocks was witnessed.

What learning can be drawn from the above examples?

Firstly, the government policies create lucrative economics for the companies. We need to study such companies in conjunction with the change in policy. The future profits, cash flows need to be estimated based on policy impact and opportunity size. If we wait for the numbers to flow in, the re-rating might have already happened and we will miss the larger gains.

Secondly, we should not have biases of past performances of these companies. The change in policy was all that these companies needed to grow. Without the change in policy, there would not have been such strong growth. Thus, we shouldn’t fixate ourselves to their past numbers which could have been poor as the environment was not conducive to growth.

Lastly, we should always keep in mind that the performance due to change in government policy cannot be taken as a given. Changes in government can lead to changes in the policies and again the economics of these businesses can turn to be subpar. We need to constantly track and keep ourselves updated with those policies.