OFSS - One off or Structural Growth?

OFSS - One off or Structural Growth?

When Elephant dances....

About the Company :

Oracle Financial Services Software Ltd (OFSS), a subsidiary of Oracle Corp, provides IT services to the financial services industry. The company provides banking software, including cloud-based solutions, banking payment solutions, revenue management, cloud infrastructure and financial services analytical applications.

History of the Company :

Oracle Corporation (US Listed Entity) purchased Citigroup's 41% stake in i-flex Solutions for US$593 million in August 2005, a further 7.52% in March and April 2006, and 3.2% in an open-market purchase in mid-April 2006.

On 14 August 2006, Oracle Financial Services announced it would acquire Mantas, a US-based anti-money laundering and compliance software company for US$122.6 million. The company part-funded the transaction through a preferential share allotment to the majority shareholder Oracle Corporation.

On 12 January 2007, after an open offer price to minority shareholders, Oracle increased its stake in I-FLEX to around 83%.

On 4 April 2008, Oracle changed the name of the company to Oracle Financial Services Limited.

In the last 10 years, the compounded sales growth of OFSS has been 5%. When compared to other product software and IT services companies this looks muted. Even the profit growth has been similar. It was looked at as a dividend yield stock.

Q3 FY 24 results were announced by the Company and it reported revenue growth of 25% and stock rose 30% on a single day. This high year on year growth for the quarter was in contrast to the historical growth rate that we discussed above.

A Shy Company

The Company does not do conference calls, share presentations or meet analysts despite being a large cap MNC & hence, analyst / brokerage coverage is minimal which is quite surprising for a company of this size!

A deeper analysis of press release filings and financials will let us understand if it was a one off growth or has there been some change in growth profile.

Let’s first understand the revenue segments of OFSS as it is important to understand the growth drivers.

OFSS earns revenue through four verticals namely -

License fees are charged on sale of the software. Users have the rights to use the software.

Maintenance fees are charged from those who purchase software licenses to keep the software up and running in good condition.

Implementation fees (Consulting fees) are charged as one-time fees associated with setting up a new software solution for the client and typically include the cost of training employees.

Services fees are charged for any other services provided.

We will have to understand the revenue recognition policy of the company too.

License fees - If only software rights are sold, revenue will be recognized immediately. In such scenarios, the implementation is done by GSIs like TCS, Accenture etc. & OFSS recognises the license fee in one shot.

But if OFSS only does the implementation and customization (added service) for the client then license fees will be Amortized i.e. recognized over the implementation period.

Hence, it reports License signed ($) & License Fee Revenue (INR) separately. And License Fee Revenue contains both the one shot & amortized revenue.Maintenance and Services fees - Recognized whenever they accrue. (very stable)

Implementation fees - The revenue is recognized using the percentage-of-completion method as the implementation is performed. (linked to implementation)

So, Why is the stock surging like never before?

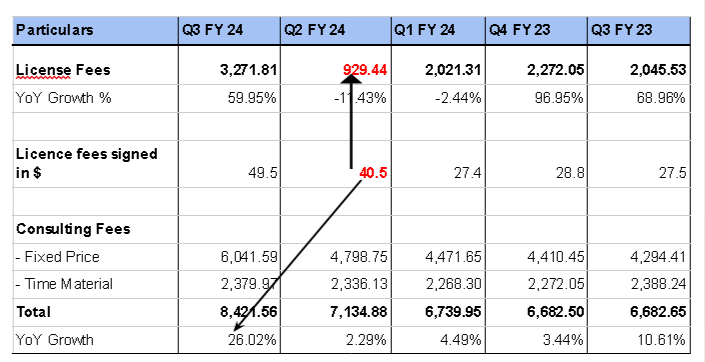

Q2 FY24:

In the last four years, for the first time in Q2 FY24, the new license agreements signed during the quarter exceeded $40 million which translates to approximately INR 382 crore. But only INR 92 crore license revenue was recognized and implementation revenue also showed growth of 2% YoY. This is where our understanding of revenue recognition policy will help us. One should have got an idea at this moment that maybe the license agreements signed include implementation work too and license revenue will be recognized over the implementation period. Hence, most of the revenue is going to be deferred. This resulted in substantially low EBITDA margins in Q2FY24

Q3 FY24:

The pace of new license agreements signed further increased to $49 million which translates to approximately INR 400 crore. License revenue for the Q3 FY24 was INR 329 crore showing growth of more than 50% YoY. The implementation revenue was INR 842 crore showing growth of 26% YoY - highest growth in last 4 years. Earlier, for a few quarters in the last four years, license revenue showed high growth YoY especially in Q1 of the FY, as is evident from the above graph but implementation revenue showed growth of less than 10% except two quarters. We can conclude that currently the company is signing license agreements with more implementation projects & hence revenue recognition is going to be backended. Significant license wins in the last two quarters provides a good visibility for implementation revenue and thus overall revenue growth.

Conclusion :

Understanding the revenue recognition policy can help us connect the dots when there is no direct communication from the management. One or two quarters of sub par financial performance may not necessarily indicate the future prospects as software product businesses are lumpy and accounting is different from pure IT service firms.

Generating alpha in lesser tracked companies is easier.

Disclaimer-

This post is purely for knowledge purposes & should not be construed as any investment recommendation. Kindly consult your investment advisor before making any investment related decision. Nimriti Investment Advisors LLP & its clients may have a vested interest in the above mentioned securities & hence our opinion could be biased.

|

TKS A LOT FOR sage article.

whats your view and advice post q4 fy 24 n fy 24 nos of OFSS anounced today ?

Thanks for the article. Can you write on valuation as well.